本文主要是介绍Re_Lasso,希望对大家解决编程问题提供一定的参考价值,需要的开发者们随着小编来一起学习吧!

from sklearn.linear_model import LassoCV, Lasso

import pandas as pd

from sklearn.model_selection import train_test_split

from sklearn.metrics import mean_absolute_error, mean_squared_error, r2_score

from sklearn.model_selection import GridSearchCV# 读取数据

df_stars = pd.read_excel('C:/Users/galax/Desktop/Final_Result.xls')

data_stars = df_stars# 属性矩阵和预测目标

X = data_stars.iloc[:, 1:14]

y = data_stars.iloc[:, 1]# 特征名称和目标名称

feature_names = ['KNN_derta_V', 'MOID', 'e', 'a', 'q', 'i', 'node', 'peri', 'M', 'tp','period', 'n', 'Price']target_name = ['Profit_numeric']# 划分训练集和测试集

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.2, random_state=19)# 创建Lasso模型

lasso_0 = Lasso(max_iter=60000)

# 拟合Lasso模型

lasso_0.fit(X_train, y_train)# 定义参数网格

param_grid = {'alpha': [0.0001, 0.0005, 0.001, 0.005, 0.01, 0.1, 1, 10, 100, 1000]

}# 使用GridSearchCV调整参数

lasso_cv = GridSearchCV(lasso_0, param_grid, cv=7, n_jobs=-1)

lasso_cv.fit(X_train, y_train)

#第三个lasso模型

lasso_cv1=Lasso(alpha=0.0001,max_iter=10000)

lasso_cv1.fit(X_train,y_train)lasso_cv2=Lasso(alpha=0.001,max_iter=10000)

lasso_cv2.fit(X_train,y_train)

lasso_cv3=Lasso(alpha=0.01,max_iter=10000)

lasso_cv3.fit(X_train,y_train)

lasso_cv4=Lasso(alpha=0.1,max_iter=10000)

lasso_cv4.fit(X_train,y_train)

lasso_cv5=Lasso(alpha=1,max_iter=10000)

lasso_cv5.fit(X_train,y_train)# 用调整后的模型做预测

y_pred_cv = lasso_cv.predict(X_test)

y_pred_cv1 = lasso_cv1.predict(X_test)

y_pred_cv2 = lasso_cv2.predict(X_test)

y_pred_cv3= lasso_cv3.predict(X_test)

y_pred_cv4 = lasso_cv4.predict(X_test)

y_pred_cv5= lasso_cv5.predict(X_test)

print("调参后,LassoCV模型的预测值为:", y_pred_cv)

print("调参后,LassoCV1模型的预测值为:", y_pred_cv1)#用3个衡量指标查看调参后的模型性能

print("平均绝对误差MAE2=",mean_absolute_error(y_test,y_pred_cv))

print("均方误差MSE2=",mean_squared_error(y_test,y_pred_cv))

print("R平方值2=",r2_score(y_test,y_pred_cv))

print("最佳的alpha=",lasso_cv.best_params_)#alpha=0.0001#用3个衡量指标查看调参后的模型性能

print("平均绝对误差MAE2=",mean_absolute_error(y_test,y_pred_cv1))

print("均方误差MSE2=",mean_squared_error(y_test,y_pred_cv1))

print("R平方值2=",r2_score(y_test,y_pred_cv1))

print("最佳的alpha=",lasso_cv.best_params_)#alpha=0.0001import matplotlib.pyplot as plt

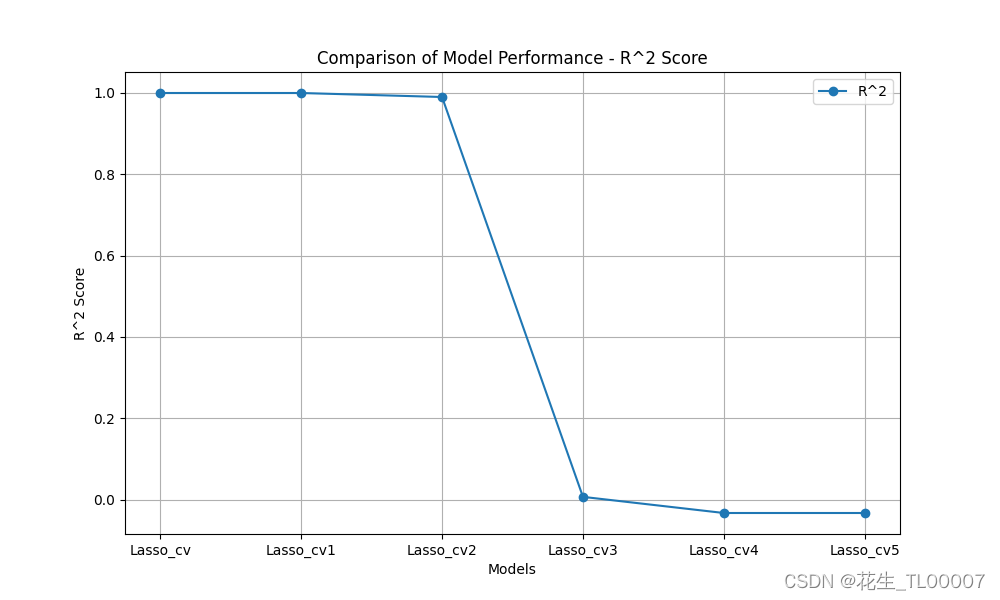

# 绘制两个lasso模型的R^2对比曲线

plt.figure(figsize=(10, 6))

plt.plot(['Lasso_cv', 'Lasso_cv1','Lasso_cv2','Lasso_cv3','Lasso_cv4','Lasso_cv5'], [r2_score(y_test, y_pred_cv), r2_score(y_test, y_pred_cv1),r2_score(y_test, y_pred_cv2),r2_score(y_test, y_pred_cv3),r2_score(y_test, y_pred_cv4),r2_score(y_test, y_pred_cv5)], marker='o', label='R^2')

plt.xlabel('Models')

plt.ylabel('R^2 Score')

plt.title('Comparison of Model Performance - R^2 Score')

plt.legend()

plt.grid(True)

plt.show()

import numpy as np

from sklearn.linear_model import LassoCV, Lasso

import pandas as pd

from sklearn.model_selection import train_test_split

from sklearn.metrics import mean_absolute_error, mean_squared_error, r2_score

from sklearn.model_selection import GridSearchCV# 读取数据

df_stars = pd.read_excel('C:/Users/galax/Desktop/Final_Result.xls')

data_stars = df_stars# 属性矩阵和预测目标

X = data_stars.iloc[:, 1:14]

y = data_stars.iloc[:, 0]# 特征名称和目标名称

feature_names = ['KNN_derta_V', 'MOID', 'e', 'a', 'q', 'i', 'node', 'peri', 'M', 'tp','period', 'n', 'Price']target_name = ['Profit']# 划分训练集和测试集

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.2, random_state=19)# 创建Lasso模型

lasso_0 = Lasso(max_iter=60000)

# 拟合Lasso模型

lasso_0.fit(X_train, y_train)# 定义参数网格

param_grid = {'alpha': [0.0001, 0.0005, 0.001, 0.005, 0.01, 0.1, 1, 10, 100, 1000]

}# 使用GridSearchCV调整参数

lasso_cv = GridSearchCV(lasso_0, param_grid, cv=7, n_jobs=-1)

lasso_cv.fit(X_train, y_train)

#第三个lasso模型

lasso_cv1=Lasso(alpha=0.0001,max_iter=10000)

lasso_cv1.fit(X_train,y_train)lasso_cv2=Lasso(alpha=0.001,max_iter=10000)

lasso_cv2.fit(X_train,y_train)

lasso_cv3=Lasso(alpha=0.01,max_iter=10000)

lasso_cv3.fit(X_train,y_train)

lasso_cv4=Lasso(alpha=0.1,max_iter=10000)

lasso_cv4.fit(X_train,y_train)

lasso_cv5=Lasso(alpha=1,max_iter=10000)

lasso_cv5.fit(X_train,y_train)# 用调整后的模型做预测

y_pred_cv = lasso_cv.predict(X_test)

y_pred_cv1 = lasso_cv1.predict(X_test)

y_pred_cv2 = lasso_cv2.predict(X_test)

y_pred_cv3= lasso_cv3.predict(X_test)

y_pred_cv4 = lasso_cv4.predict(X_test)

y_pred_cv5= lasso_cv5.predict(X_test)

print("调参后,LassoCV模型的预测值为:", y_pred_cv)

print("调参后,LassoCV1模型的预测值为:", y_pred_cv1)#用3个衡量指标查看调参后的模型性能

print("平均绝对误差MAE2=",mean_absolute_error(y_test,y_pred_cv))

print("均方误差MSE2=",mean_squared_error(y_test,y_pred_cv))

print("R平方值2=",r2_score(y_test,y_pred_cv))

print("最佳的alpha=",lasso_cv.best_params_)#alpha=0.0001#用3个衡量指标查看调参后的模型性能

print("平均绝对误差MAE2=",mean_absolute_error(y_test,y_pred_cv1))

print("均方误差MSE2=",mean_squared_error(y_test,y_pred_cv1))

print("R平方值2=",r2_score(y_test,y_pred_cv1))

print("最佳的alpha=",lasso_cv.best_params_)#alpha=0.0001import matplotlib.pyplot as plt

# 绘制两个lasso模型的R^2对比曲线

plt.figure(figsize=(10, 6))

plt.plot(['Lasso_cv', 'Lasso_cv1','Lasso_cv2','Lasso_cv3','Lasso_cv4','Lasso_cv5'], [r2_score(y_test, y_pred_cv), r2_score(y_test, y_pred_cv1),r2_score(y_test, y_pred_cv2),r2_score(y_test, y_pred_cv3),r2_score(y_test, y_pred_cv4),r2_score(y_test, y_pred_cv5)], marker='o', label='R^2')

plt.xlabel('Models')

plt.ylabel('R^2 Score')

plt.title('Comparison of Model Performance - R^2 Score')

plt.legend()

plt.grid(True)

plt.show()lasso_x=Lasso(alpha=0.1)

#计算Lasso回归路径

alphas=np.logspace(-3,0,100)

coefs=[]

for a in alphas:lasso_x.set_params(alpha=a)lasso_x.fit(X_train, y_train)coefs.append(lasso_x.coef_)

#绘制lasso回归路径图

plt.figure(figsize=(10, 6))

ax=plt.gca()

ax.plot(alphas, coefs, marker='o', label='Lasso_x')

ax.set_xscale('log')

ax.set_xlim(ax.get_xlim()[::-1])

plt.xlabel('alpha')

plt.ylabel('weights')

plt.axis('tight')

plt.show()#绘制LASSO系数图

plt.bar(range(len(lasso_x.coef_)), lasso_x.coef_)

plt.xticks(range(len(lasso_x.coef_)), feature_names)

plt.show()这篇关于Re_Lasso的文章就介绍到这儿,希望我们推荐的文章对编程师们有所帮助!