本文主要是介绍期货日数据维护与使用_日数据维护_主力合约计算逻辑,希望对大家解决编程问题提供一定的参考价值,需要的开发者们随着小编来一起学习吧!

目录

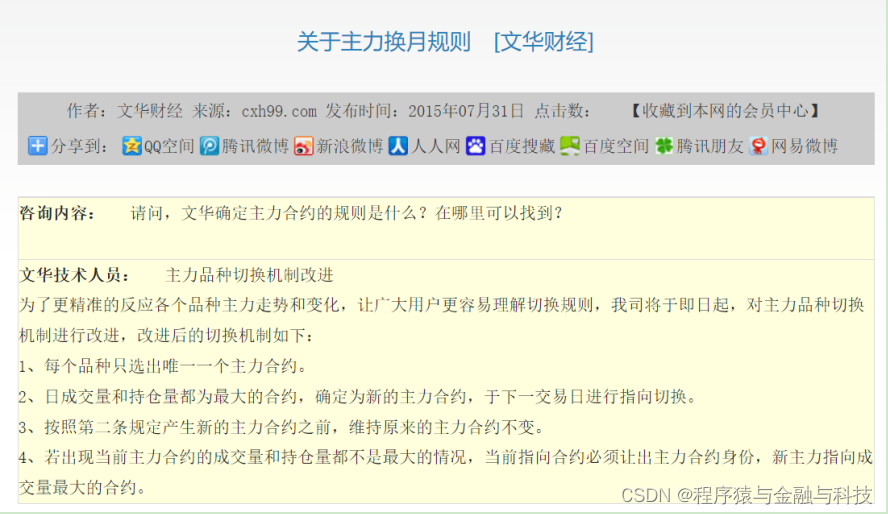

主力合约换月规则(文化财经)

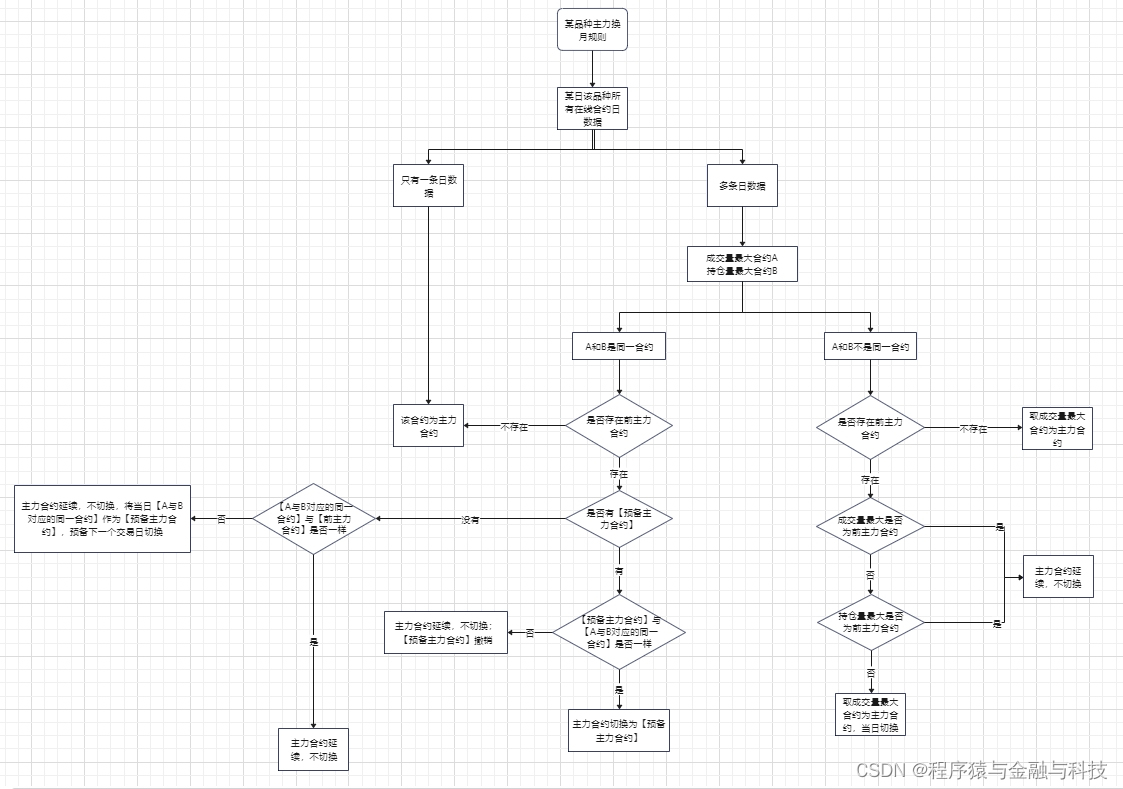

主力合约计算逻辑

数据准备

代码

下载

主力合约换月规则(文化财经)

主力合约计算逻辑

数据准备

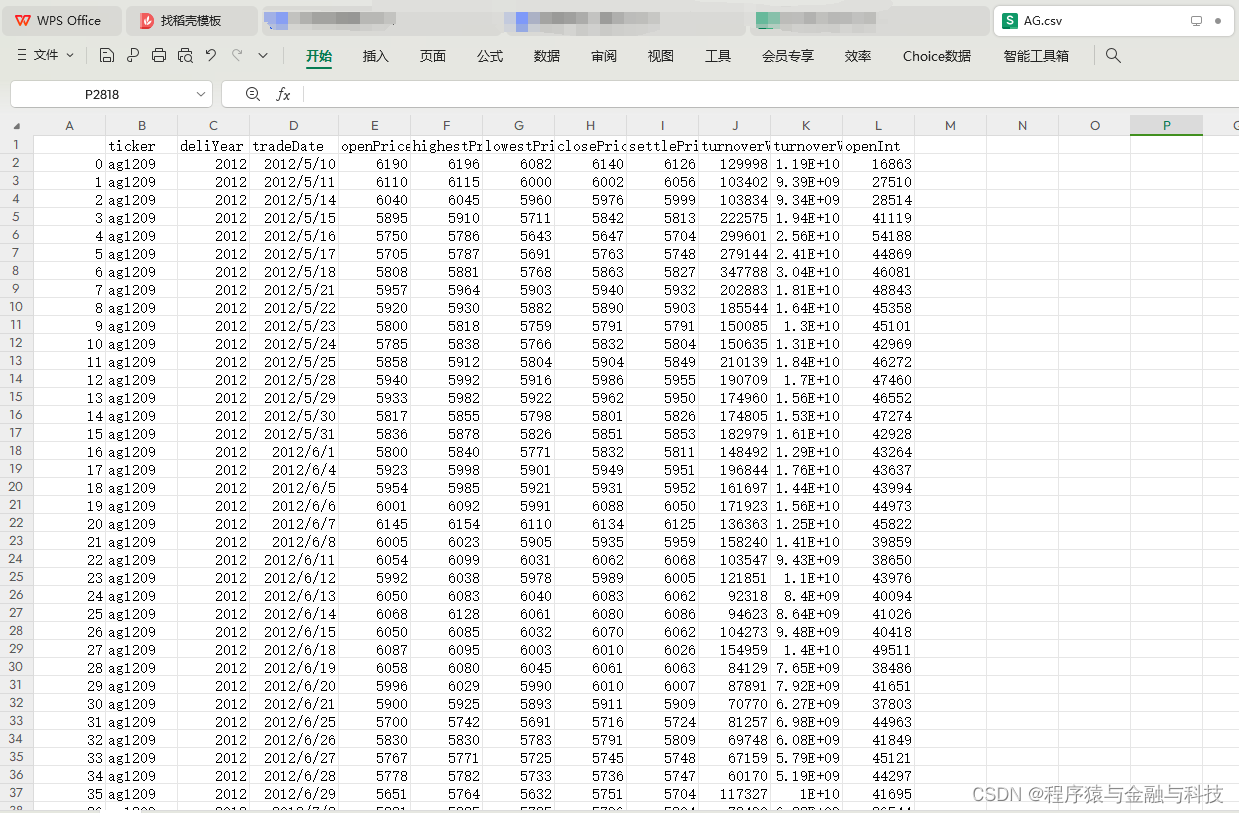

本文以沪银为例,将沪银所有日数据文件放入一个文件夹中,文件名命名方式为 合约名_交割年份.csv

代码

def caculate_main_from_zero():main_column_list = ['ticker','deliYear','tradeDate','openPrice','highestPrice','lowestPrice','closePrice','settlePrice','turnoverVol','turnoverValue','openInt']# 放置品种所有日数据文件,文件名 合约名_交割年份.csvpre_dir = r'E:/temp000/'file_list = os.listdir(pre_dir)# 将合约日文件合并到一个pd.DataFrame()中df = pd.DataFrame()for item in file_list:file_path = pre_dir + itemitem_str = item.split('.')[0]ticker = item_str.split('_')[0]deliYear = item_str.split('_')[1]df_one = pd.read_csv(file_path,encoding='utf-8')df_one['ticker'] = tickerdf_one['deliYear'] = deliYeardf = pd.concat([df,df_one])pass# 去除数据为空的数据df.dropna(inplace=True)if len(df)<=0:print('所有合约数据为空')return# 按日期分组df['o_date'] = pd.to_datetime(df['tradeDate'])df.sort_values(by='o_date',ascending=True,inplace=True)df['row_i'] = [i for i in range(len(df))]df_group = df.groupby(by='o_date',as_index=False)df_main = pd.DataFrame()cur_main_ticker = Nonecur_main_deliYear = Nonepre_next_ticker = Nonepre_next_deliYear = Nonenext_change_yeah = Falsefor name,group in df_group:if len(group)<=1:# 当日只有一条日数据,那该数据对应的合约即为主力合约df_main = pd.concat([df_main,group.iloc[[0]]])cur_main_ticker = group.iloc[0]['ticker']cur_main_deliYear = group.iloc[0]['deliYear']passelse:# 当日有多条日数据,分别计算成交量最大和持仓量最大的合约# 成交量最大合约df_vol = group.sort_values(by='turnoverVol',ascending=False)# 持仓量最大合约df_inte = group.sort_values(by='openInt',ascending=False)# 如果成交量最大与持仓量最大为同一合约if df_vol.iloc[0]['row_i'] == df_inte.iloc[0]['row_i']:if not cur_main_ticker:# 不存在前主力合约,那该合约即为主力合约df_main = pd.concat([df_main,df_vol.iloc[[0]]])cur_main_ticker = df_vol.iloc[0]['ticker']cur_main_deliYear = df_vol.iloc[0]['deliYear']passelse:if next_change_yeah:# 有【预备主力合约】if df_vol.iloc[0]['ticker'] == pre_next_ticker and df_vol.iloc[0]['deliYear']==pre_next_deliYear:# 【预备主力合约】继昨日是成交量和持仓量同时最大后,今日还是成交量和持仓量最大,切换df_main = pd.concat([df_main, df_vol.iloc[[0]]])cur_main_ticker = pre_next_tickercur_main_deliYear = pre_next_deliYearnext_change_yeah = Falsepasselse:# 【预备主力合约】继昨日是成交量和持仓量同时最大后,今日不济,【预备主力合约】撤销next_change_yeah = False# ----------- 【当日成交量最大和持仓量最大 为同一个合约】 延续当前合约 start# 存在前主力合约,判断该合约是否与前主力合约一致if df_vol.iloc[0]['ticker'] == cur_main_ticker and df_vol.iloc[0]['deliYear'] == cur_main_deliYear:# 一致,主力合约延续,不切换df_main = pd.concat([df_main, df_vol.iloc[[0]]])passelse:# 不一致,主力合约延续,不切换;预备下一交易日切换one_df = group.loc[(group['ticker'] == cur_main_ticker) & (group['deliYear'] == cur_main_deliYear)].copy()df_main = pd.concat([df_main, one_df.iloc[[0]]])next_change_yeah = Truepre_next_ticker = df_vol.iloc[0]['ticker']pre_next_deliYear = df_vol.iloc[0]['deliYear']pass# ----------- 【当日成交量最大和持仓量最大 为同一个合约】 延续当前合约 endpasspasselse:# 无【预备主力合约】# ----------- 【当日成交量最大和持仓量最大 为同一个合约】 延续当前合约 start# 存在前主力合约,判断该合约是否与前主力合约一致if df_vol.iloc[0]['ticker'] == cur_main_ticker and df_vol.iloc[0]['deliYear'] == cur_main_deliYear:# 一致,主力合约延续,不切换df_main = pd.concat([df_main, df_vol.iloc[[0]]])passelse:# 不一致,主力合约延续,不切换;预备下一交易日切换one_df = group.loc[(group['ticker'] == cur_main_ticker) & (group['deliYear'] == cur_main_deliYear)].copy()df_main = pd.concat([df_main, one_df.iloc[[0]]])next_change_yeah = Truepre_next_ticker = df_vol.iloc[0]['ticker']pre_next_deliYear = df_vol.iloc[0]['deliYear']pass# ----------- 【当日成交量最大和持仓量最大 为同一个合约】 延续当前合约 endpasspasselse:# 成交量最大和持仓量最大不是同一合约if not cur_main_ticker:df_main = pd.concat([df_main,df_vol.iloc[[0]]])cur_main_ticker = df_vol.iloc[0]['ticker']cur_main_deliYear = df_vol.iloc[0]['deliYear']passelse:if df_vol.iloc[0]['ticker']==cur_main_ticker and df_vol.iloc[0]['deliYear']==cur_main_deliYear:df_main = pd.concat([df_main,df_vol.iloc[[0]]])elif df_inte.iloc[0]['ticker'] == cur_main_ticker and df_inte.iloc[0]['deliYear']==cur_main_deliYear:df_main = pd.concat([df_main,df_inte.iloc[[0]]])else:df_main = pd.concat([df_main,df_vol.iloc[[0]]])cur_main_ticker = df_vol.iloc[0]['ticker']cur_main_deliYear = df_vol.iloc[0]['deliYear']passpasspasspasspassif len(df_main) <=0:print('主力合约条数为0')returndf_main = df_main.loc[:,main_column_list].copy()df_main.to_csv(pre_dir + 'AG.csv',encoding='utf-8')pass结果存储为 AG.csv

下载

下载

链接:https://pan.baidu.com/s/1X0O4ZtwX8_ZmdDJB4DJXTA

提取码:jjdz

这篇关于期货日数据维护与使用_日数据维护_主力合约计算逻辑的文章就介绍到这儿,希望我们推荐的文章对编程师们有所帮助!