本文主要是介绍me和adr_对交易ADR和间谍,希望对大家解决编程问题提供一定的参考价值,需要的开发者们随着小编来一起学习吧!

me和adr

算法交易(Algo Trading)

Note from Towards Data Science’s editors: While we allow independent authors to publish articles in accordance with our rules and guidelines, we do not endorse each author’s contribution. You should not rely on an author’s works without seeking professional advice. See our Reader Terms for details.

Towards Data Science编辑的注意事项:尽管我们允许独立作者按照我们的规则和指南发表文章,但我们不认可每位作者的贡献。 您不应在未征求专业意见的情况下依赖作者的作品。 有关详细信息,请参见我们的阅读器条款。

美国存托凭证(ADR) (American Depositary Receipts (ADRs))

Foreign company stocks listed in US exchanges are commonly registered as American Depositary Receipts (ADRs). These are certificates, denominated in U.S. dollars, that represent shares of non-U.S. company securities. There are about 2000 ADRs traded on U.S. exchanges, namely NYSE and NASDAQ, or through the over-the-counter (OTC) market, representing shares of companies from at least 70 different countries.

在美国交易所上市的外国公司股票通常被注册为美国存托凭证(ADR) 。 这些是以美元计价的凭证,代表非美国公司股票的份额。 在美国证券交易所(即纽约证券交易所和纳斯达克)或通过场外交易(OTC)市场交易的美国存托凭证大约有2000种,代表了至少70个不同国家的公司股票。

ADRs are among the most direct and popular financial instruments for investing in foreign companies, and have been actively used to diversify portfolios. In 2015, foreign equity holdings — through ADRs and local shares — accounted for 19% of U.S. investors’ equity portfolios.

ADR是投资外国公司最直接,最受欢迎的金融工具之一,并且已被积极用于分散投资组合。 2015年,通过美国存托凭证和本地股票持有的外国股票占美国投资者股票投资组合的19%。

Specifically, total global investments in DRs, both American and non-American, were estimated to be approximately $1 trillion USD, with about 90% specifically in ADRs, according to reports by JP Morgan. Some of the most traded ETFs are comprised of ADRs as well. For instance, 14 Chinese ADRs were added to the MSCI Emerging Market Index in late 2015. The iShares MSCI Emerging Markets ETF (EEM), which tracks this index, has a market capitalization of $24 billion and daily average volume of 72 million shares.

具体来说,据摩根大通的报告,全球对美国和非美国存托凭证的总投资估计约为1万亿美元,其中约90%专门用于ADR。 一些交易量最大的ETF也包括ADR。 例如,2015年底,有14个中国ADR加入了MSCI新兴市场指数。追踪该指数的iShares MSCI新兴市场ETF(EEM)市值为240亿美元,日平均交易量为7200万股。

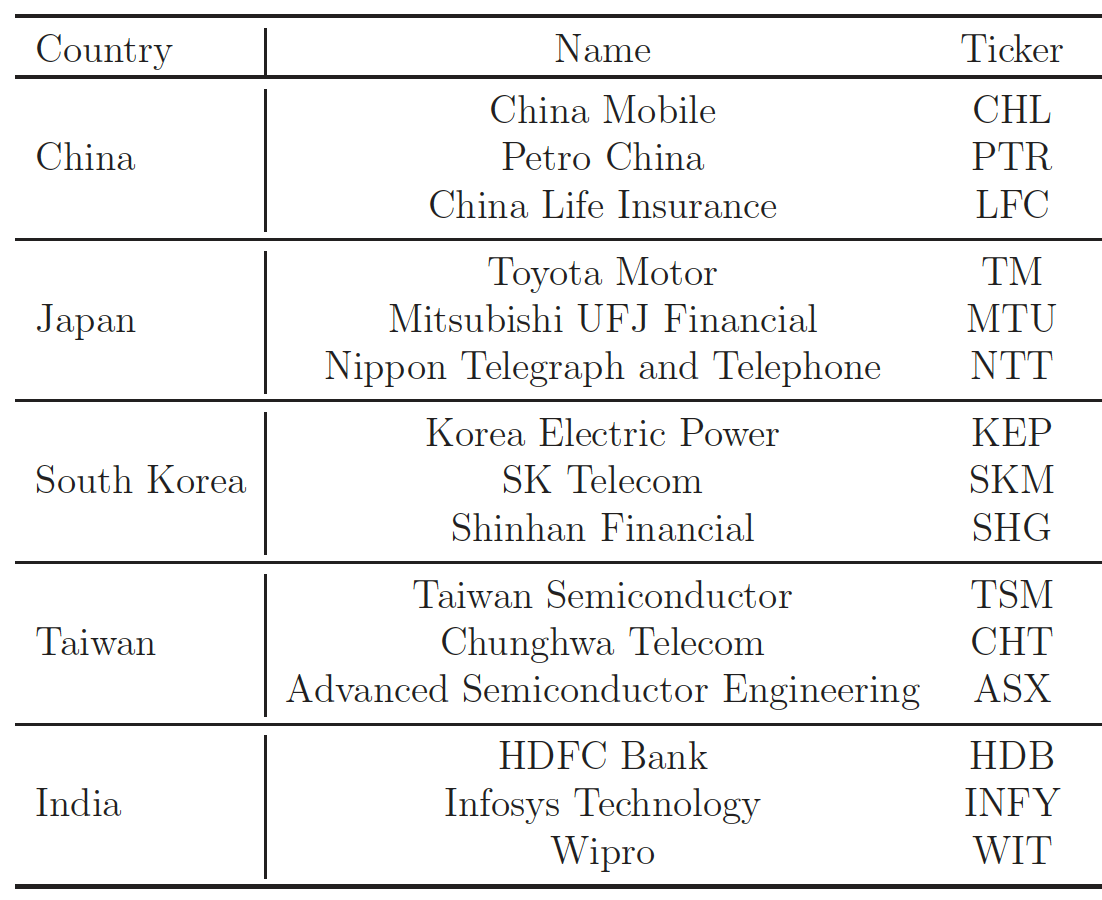

Due to their cross-border nature, ADRs’ returns are significantly dependent on the market sentiments of both the U.S. and originating home markets. Especially, ADRs from Asia, such as Japan, Hong Kong, China, Taiwan, India, and Korea, are of particular interest.

由于其跨境性质,ADR的回报很大程度上取决于美国和原始市场的市场情绪。 特别是来自亚洲的ADR ,例如日本,香港,中国大陆,台湾,印度和韩国,尤其引起人们的关注。

These ADRs provide U.S. investors with direct viable means to invest in foreign and emerging markets. Consequently, Asian DRs listed on non-Asian exchanges accounted for over 44% of the total DR market capitalization.

这些ADR为美国投资者提供了直接可行的手段来投资于外国和新兴市场。 因此,在非亚洲交易所上市的亚洲存托凭证占总存托凭证市值的44%以上。

不重叠的时区 (Nonoverlapping Time Zones)

The time zones for the aforementioned countries are 12-14 hours ahead of New York’s Eastern Standard Time (EST). Therefore, the trading hours of the U.S. market and their home markets do not overlap. The originating home markets open after the U.S. market closes and vice versa.

上述国家/地区的时区比纽约的东部标准时间(EST)早12-14小时。 因此,美国市场及其本国市场的交易时间不会重叠。 美国市场收盘后,原始国内市场开放,反之亦然。

This leads to asynchronicity in the ADR returns with respect to their underlying equities (in their home countries). Completely asynchronous markets are particularly interesting to multi-asset investors and other institutional investors.

这导致了异步性 美国存托凭证回报率(在其母国)与其基础股票有关。 完全异步市场对于多资产投资者和其他机构投资者特别有趣。

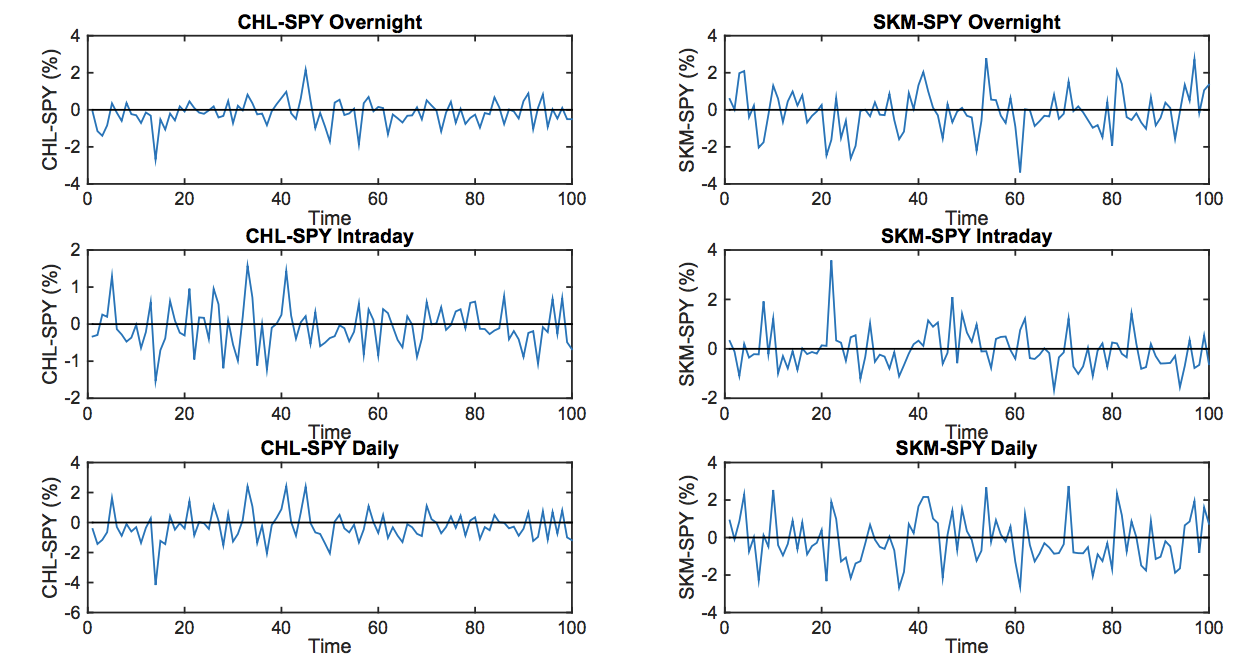

Similarly, the time zone discrepancy allows us to split their returns into intraday and overnight components, each with fundamentally different price driving factors. For the ADRs studied herein, intraday returns can be intuitively attributed to the news, conditions, and outlook of the U.S. market, whereas overnight returns are predominantly driven by the local Asian markets. The volatility contribution from each market is of interest here.

同样,时区差异使我们可以将其收益分成当日和隔夜部分,每个部分具有根本不同的价格驱动因素。 对于本文研究的ADR,日内收益可以直观地归因于美国市场的新闻,状况和前景,而隔夜收益主要由亚洲本地市场驱动。 每个市场的波动性贡献在这里都很有趣。

返回:隔夜vs日内 (Returns: Overnight vs Intraday)

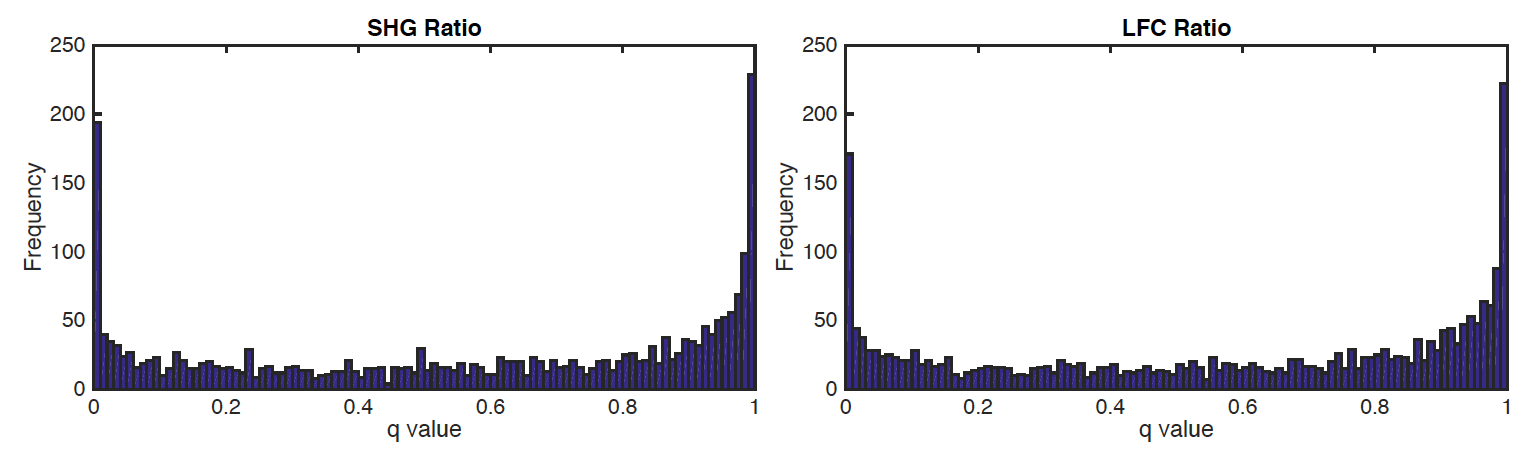

We compare the daily proportion of overnight returns in terms of the squared returns ratio defined by

我们根据隔夜收益率的平方比来比较隔夜收益的每日比例

on each day i. Typically, the average value fo this ratio is above 0.5 for most ADRs but well lower than 0.5 for SPY. A higher ratio implies that overnight returns have more variations than intraday returns.

每一天我。 通常,对于大多数ADR,该比率的平均值高于0.5,但对于SPY,平均值却远低于0.5。 较高的比率意味着隔夜收益比日内收益变化更大。

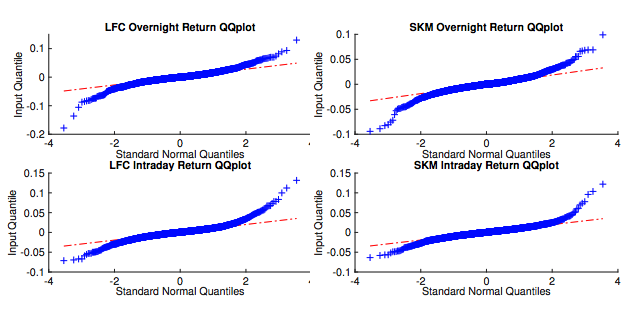

In Kang and Leung (2016) we present other salient characteristics of ADRs, including the key statistics of the intraday returns and overnight returns, their distributions and correlations with the U.S. market.

在Kang and Leung(2016)中,我们介绍了ADR的其他显着特征,包括日内收益和隔夜收益的主要统计数据,它们的分布以及与美国市场的相关性。

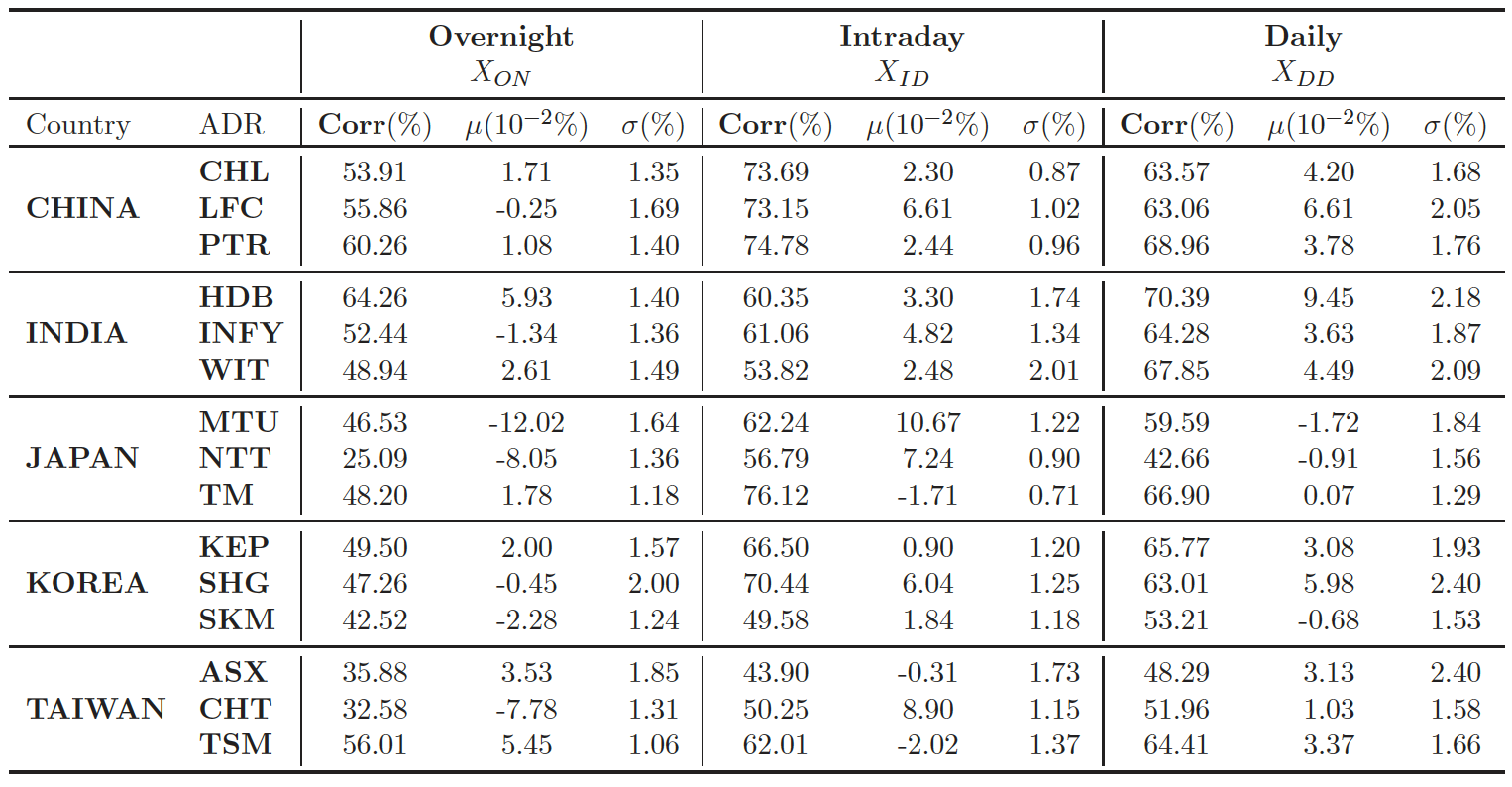

The correlation of each ADR with respect to the U.S. market is useful since it can serve as the basis of some trading strategies. Since intraday returns reflect price fluctuations during the U.S. market hours, they are expected to have a relatively high correlation with the U.S. market returns. On a similar note, overnight returns are expected to have a significantly lower correlation. The study determines these correlations, quantitatively contrast their effects on the overall volatility and performance of each ADR.

每个ADR与美国市场之间的相关性很有用,因为它可以作为某些交易策略的基础。 由于盘中收益反映了美国市场时段的价格波动,因此预计它们与美国市场收益具有相对较高的相关性。 同样,隔夜收益预计具有显着较低的相关性。 该研究确定了这些相关性,定量地比较了它们对每种ADR的整体波幅和性能的影响。

均值回差 (Mean-Reverting Spread)

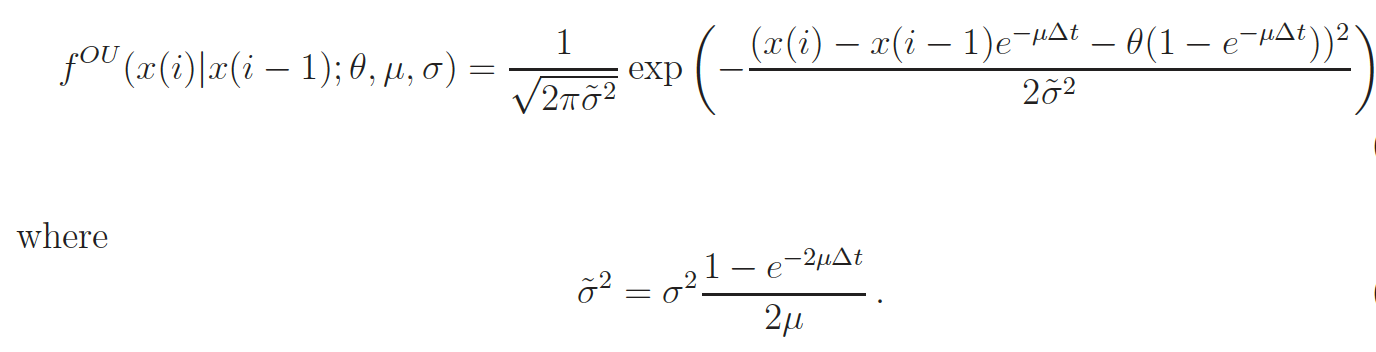

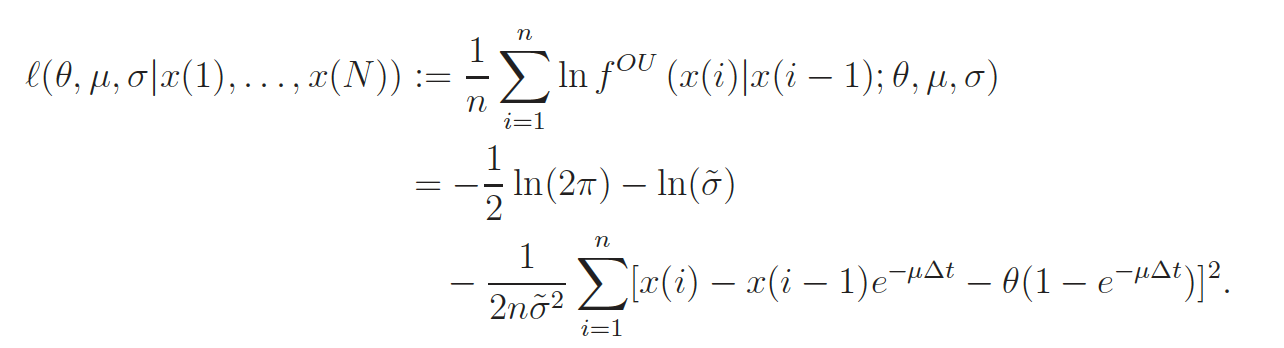

The return difference between the S&P500 index, traded through the SPDR S&P500 ETF (SPY), and each ADR is found to be a mean-reverting time series, and is fitted to an Ornstein-Uhlenbeck process via maximum-likelihood estimation (MLE).

通过SPDR S&P500 ETF(SPY)交易的S&P500指数与每个ADR之间的收益差被发现是一个均值回复时间序列,并通过最大似然估计(MLE)拟合到Ornstein-Uhlenbeck过程。

We model the return spreads by an Ornstein-Uhlenbeck process, described by the stochastic differential equation

我们通过随机微分方程描述的Ornstein-Uhlenbeck过程对收益点差进行建模

We can then express the conditional probability of the spread at time step i given the previous data at time i-1 as

在给定时间i-1之前的数据的情况下,我们可以将时间步i的扩展的条件概率表示为

An observation of the sequence (x(1), x(2), . . . , x(N)) allows us to compute, and thereby maximize the average log-likelihood defined by

对序列(x(1),x(2),...,x(N))的观察使我们能够进行计算,从而最大化由定义的平均对数似然

点差交易 (Spread Trading)

To exploit the mean-reverting ADR-SPY spreads, pairs trading strategies (long position in ADR and short position in SPY) are introduced and backtested.

为了利用均值回复的ADR-SPY价差,引入并回测配对交易策略(ADR中的多头头寸和SPY中的空头头寸)。

In our pairs trading strategy, we long ADR and short SPY. We choose SPY to short because it is significantly more liquid than ADRs and is much easier to borrow.

在我们的货币对交易策略中,我们多头ADR和空头SPY 。 我们选择SPY做空,因为它比ADR流动性大得多,而且借用容易得多。

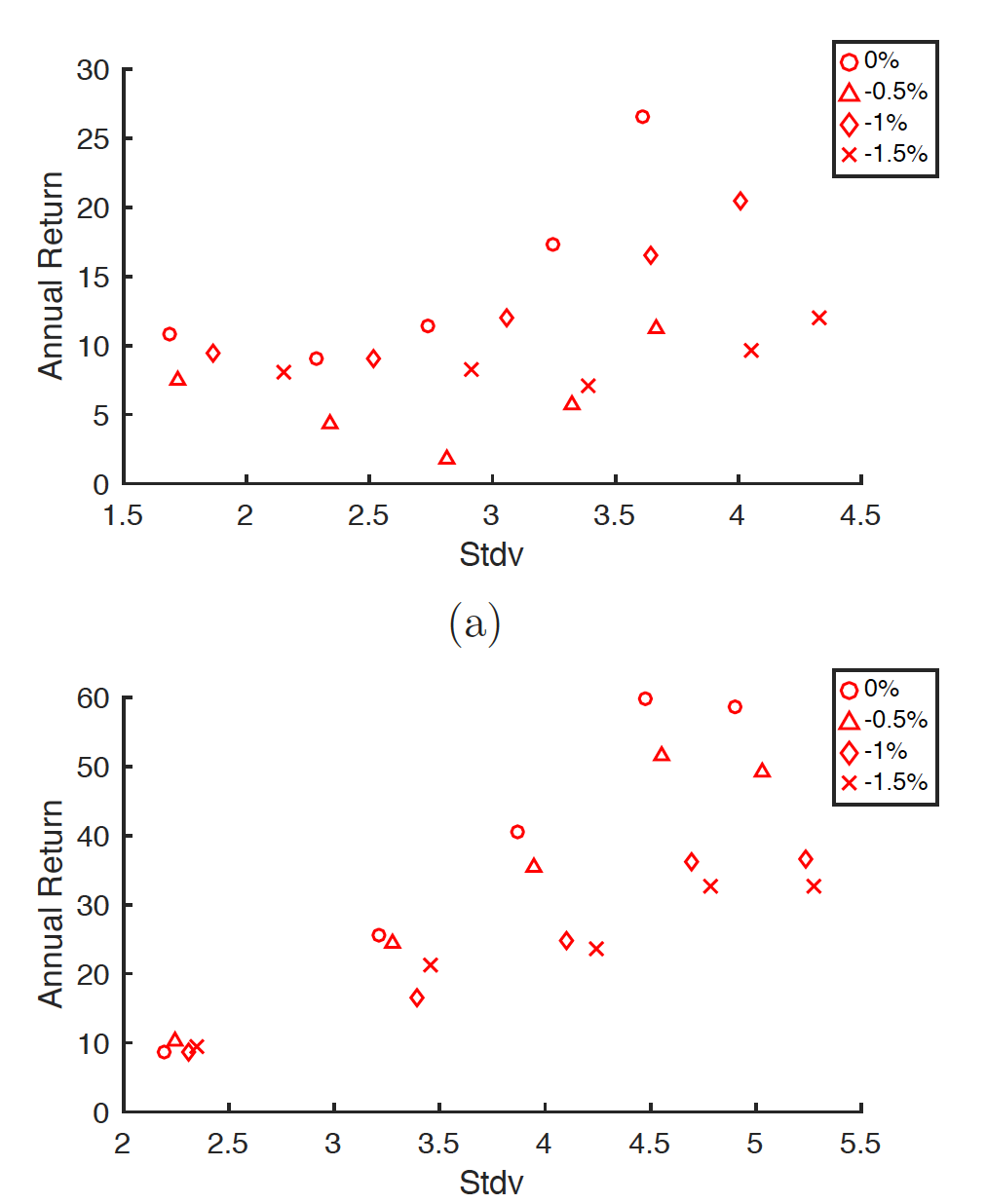

For an optimal result we set a specific entry level threshold and enter the given position when the return spread, ADR-SPY, is below this certain threshold value k%.

为了获得最佳结果,我们设置了一个特定的入门水平阈值,并在收益差价ADR-SPY低于此特定阈值k %时输入给定位置。

We assume here that both long and short positions are worth $100, resulting in zero net cash outflow. Therefore, we report returns not in percentages, but instead in the cash values of their payoffs. We examine the pairs trading strategy by varying the entry threshold from 0% to -1.5% with a -0.5% step and the number of days to liquidate from 1 to 5 days.

在此我们假设多头和空头头寸ASP值100美元,导致净现金流出为零。 因此,我们报告的回报率不是百分比,而是回报的现金价值。 我们通过将入场门槛值从0%更改为-1.5%(步长为-0.5%)并将清算天数从1天更改为5天来研究交易对策略。

The paper is available in pdf here: https://ssrn.com/abstract=2858048

该文件可通过pdf下载: https : //ssrn.com/abstract=2858048

翻译自: https://towardsdatascience.com/pairs-trading-adr-and-spy-b460c498025b

me和adr

相关文章:

这篇关于me和adr_对交易ADR和间谍的文章就介绍到这儿,希望我们推荐的文章对编程师们有所帮助!